1. Introduction

Wood pulp is the main component in the papermaking process. The pulp and paper industry in Korea depends heavily on imported pulp for the manufacturing of various paper products. In 2017, the volume of pulp consumed was 2,738,179 metric tons, of which 82.8% was imported and 86.3% was chemical pulp.

It is well known that the wood pulp market is highly volatile. In fact, it has become increasingly unstable. Wood pulp costs directly impact paper prices, and ultimately impact the profitability of the pulp and paper industry. An increase in wood pulp price leads to decreasing profits for paper companies that buy wood pulp as raw material. Thus, paper companies face the risk of rising pulp prices. On the other hand, a decrease in wood pulp price leads to decreasing profits for pulp companies that sell wood pulp as the final product. Thus, pulp companies face the risk of falling pulp prices. Effective price risk management is critical for the pulp and paper industry.

When it comes to hedging price risk in commodities, the most commonly used derivative instruments are futures contracts. While paper companies that use wood pulp can hedge against increasing wood pulp prices through buying wood pulp futures contracts, pulp companies that produce wood pulp can hedge against decreasing wood pulp prices by selling wood pulp futures contracts. Unfortunately, there is no viable futures market for wood pulp, consequently pulp and paper companies cannot directly hedge their price risks in the wood pulp futures market.[1] However, there is a wood-related futures contract traded in the Chicago Mercantile Exchange (CME), CME random length lumber futures. Thus, pulp and paper companies may have the opportunity to cross hedge wood pulp prices with CME random length lumber futures contract.[2]

This paper aims to determine the feasibility of cross hedging wood pulp with CME random length lumber futures. In order for the CME lumber futures to be used as a potential cross hedging vehicle for wood pulp, there should be close price correlations between wood pulp and CME lumber futures. In other words, they should have similar price movements.

2. Materials and Methods

2.1 Data

Cash prices for wood pulp are obtained from the Korean Statistical Information Service (KOSIS). The cash prices are monthly average prices for LBKP (laubholz bleached kraft pulp) and NBKP (nadelholz bleached kraft pulp) respectively. While LBKP is the hardwood kraft pulp made from trees with leaves, NBKP is the softwood kraft pulp made from trees with needles. The prices are based on cost, insurance and freight (CIF) values for imported wood pulp and quoted in dollars per ton ($/t).

Futures prices are the daily settlement prices of the CME random length lumber futures (RLLF).[3] The futures prices are obtained from a computer database compiled by Reuters. Since cash prices are monthly average prices, monthly averages of the nearby futures price series are used for futures prices. When constructing nearby futures price series by continuously connecting the nearby futures prices, we roll over to the next nearest contract on the last trading day (LTD) of CME RLLF.

The sample period extends from January 2003 through June 2019, resulting in 198 observations. The natural logarithms of the prices multiplied by 100 are used, since both cash and futures returns are conventionally assumed to follow log-normal distributions.

2.2 Methods and procedures[4]

2.2.1 Unit root test

A unit root test is used to test whether a time series variable is non-stationary and possesses a unit root. The presence of a unit root is tested by employing the ADF (augmented Dickey-Fuller) test using Eq. 1. The null hypothesis is that the time series has a unit root and is non-stationary.

where yt=(St, Ft), St is the cash price for LBKP and NBKP respectively, and Ft is the CME RLLF price. t represents a time trend, and ∆ represents a differencing operator such that ∆yt=yt-yt-1.

2.2.2 Cointegration test

Given that two time series variables are integrated of order one, or I(1), respectively, a cointegration test is used to test whether they share a common stochastic trend. To determine the cointegration relationship or long-run equilibrium relationship between wood pulp and CME lumber futures prices, the Johansen’s multivariate cointegration procedure is used. The Johansen approach proceeds with the general form of a pth order vector autoregressive (VAR) model.

where yt is a vector consisting of the cash price (St) for LBKP and NBKP, respectively, and the CME RLLF price (Ft). δ is a vector of constants. εt is a vector of error terms satisfying the multivariate normal white noise process with mean 0 and finite covariance matrix Σ.

The VAR(p) above can be reparameterized into a vector error correction model (VECM) of the following form.

Where

Johansen3) shows that the coefficient matrix Π contains essential information about the cointegrating or equilibrium relationship between the variables. Specifically, the rank of Π matrix is equal to the number of independent cointegrating vectors. Based on the mathematical properties that the rank of a matrix is equal to the number of its characteristic roots (eigenvalues) that differ from zero, the test for cointegration between the variables can be conducted using the following maximum eigenvalue test (λmax) statistics.

The maximum eigenvalue statistic (λmax) tests the null hypothesis that the number of cointegrating vectors is r against an alternative hypothesis of r+1 cointegrating vectors. In this study, yt=(St,Ft)' and so the number of variables is 2. The hypothesis of cointegration between St and Ft is equivalent to the hypothesis that r=1. If r=0, then the two variables are not cointegrated.

2.2.3 Vector autoregressive (VAR) model and granger causality

The temporal relationship between the variables can be studied simultaneously by estimating the vector autoregressive (VAR) model. In order to determine the price discovery and lead-lag relationship between the wood pulp and CME RLLF prices, the following VAR model is estimated.

where ∆ denotes the differencing operator. ∆St is the change in cash price for LBKP and NBKP respectively, and ΔFt is the change in CME RLLF price. εst and εft denote white noise errors with zero mean and constant variance.

In Eqs. 5-6, Granger causality tests are associated with tests on the significance of the coefficients γsj and the βfi conditional on the optimal lag length m.[5] In Eq. 5, if all the coefficients of γsj are equal to zero, implying that past changes of Ft have no explanatory power for the current change of St, then Ft does not Granger cause St. This is formally tested using the null hypothesis H0 : γs1 = γs2 = ⋯ = γfm = 0 and concluded that Ft Granger causes St if the hypothesis is rejected.

Similarly, in Eq. 6, if all the coefficients of βfi are equal to zero, implying that past changes of St have no explanatory power for the current change of Ft, then St does not Granger cause Ft. This is formally tested using the null hypothesis H0 : βf1 = βf2 = ⋯ = βfm = 0 and concluded that St Granger causes Ft if the hypothesis is rejected.

2.2.4 Estimation of the cross hedge ratio and hedging effectiveness

To estimate the risk-minimizing cross hedge ratio, a conventional method that estimates the following linear regression model is used.4)

where ∆St is the change in cash price for LBKP and NBKP respectively, ΔFt is the change in CME RLLF price, and εt is random error term.

The ordinary least squares (OLS) estimator of β1 provides an estimate for the risk-minimizing cross hedge ratio. From the estimated regression model, a measure of hedging effectiveness, R2, is also obtained. R2 is the proportion of the total variation in the wood pulp price changes statistically related to the CME RLLF price changes. Unless the cash and futures prices are closely related to each other, the cross hedging effectiveness would be very low.

3. Results and Discussion

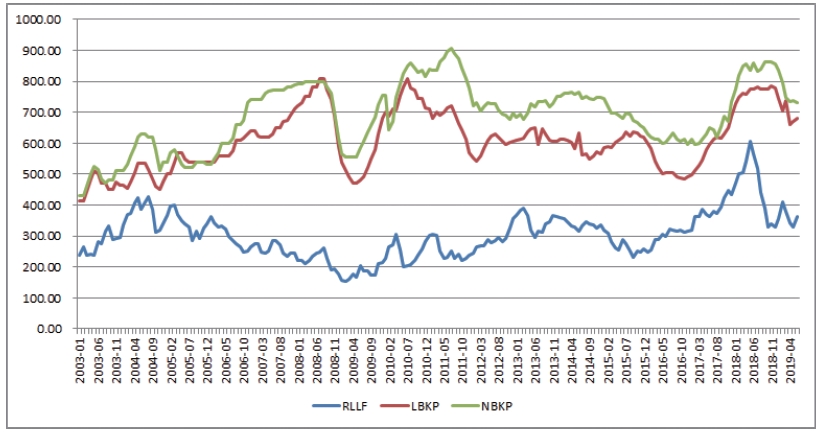

Fig. 1. illustrates the movements of the wood pulp price (NBKP on the upper line and LBKP on the middle line) and CME RLLF price (on the lower line) over the period of January 2003 through June 2019. Visual inspection of the graph does not suggest that wood pulp price and CME lumber futures price tend to move together over time. This is later confirmed using rigorous statistical tests.

Fig. 1.

Movements of the wood pulp (LBKP, NBKP) price and CME random length lumber futures (RLLF) price, January 2003 through June 2019.

3.1 Results of unit root tests

Table 1 presents the results of the ADF test to determine the presence of a unit root in the prices of wood pulp (LBKP and NBKP) and CME RLLF. While the null hypothesis of a unit root (or non-stationarity) can not be rejected in price levels, the ADF test performed on the first differences indicates that the first difference of each series is stationary. The results confirm that both the wood pulp and CME lumber futures price series are difference stationary, or I(1), integrated of order one.

3.2 Results of Johansen cointegration tests

Table 2 reports the results of Johansen cointegration tests for two pairs of price series, in other words, LBKP vs. RLLF, and NBKP vs. RLLF. The maximum eigenvalue (λmax) statistics indicate that the null hypothesis of r=0 (no cointegration) cannot be rejected at the 5% significance level. The results show evidence of zero cointegrating vector between the two price series, suggesting that there exists no cointegration or long-run equilibrium relationship between the wood pulp (LBKP and NBKP) and CME RLLF.

Table 2.

Results of Johansen cointegration tests

| LBKP vs. RLLF | NBKP vs. RLLF | |||||||

|---|---|---|---|---|---|---|---|---|

| H0 | HA | λmax | Critical value | H0 | HA | λmax | Critical value | |

| r=0 | r=1 | 12.13 | 14.26 | r=0 | r=1 | 10.22 | 14.26 | |

| r=1 | r=2 | 3.99 | 3.84 | r=1 | r=2 | 4.21 | 3.84 | |

1) Critical values are obtained from MacKinnon et al.5)

3.3 Results of vector autoregressive (VAR) model and granger causality

Table 3 presents the results of the vector autoregressive (VAR) model between LBKP and RLLF, and Granger causality test. On the left-hand side of Table 3, the coefficients of lagged terms ΔRLLFt-j are not statistically significant at all. The result indicates that the lumber futures market does not lead the wood pulp (LBKP) market in the lead-lag relationships. The Granger causality test also fails to reject the null hypothesis that RLLF does not Granger cause LBKP.

Table 3.

Results of vector autoregressive (VAR) model and granger causality

(LBKP vs. RLLF)

| Variable | ΔLBKPt | ΔRLLFt | |||

|---|---|---|---|---|---|

| Coefficient | t-statistic | Coefficient | t-statistic | ||

| Intercept | 24.0770 | 2.06* | 64.6475 | 2.53* | |

| ΔLBKPt-1 | 1.3136 | 19.52** | 0.1787 | 1.22 | |

| ΔLBKPt-2 | -0.3606 | -5.43** | -0.2264 | -1.56 | |

| ΔRLLFt-1 | 0.0310 | 0.95 | 1.1179 | 15.74** | |

| ΔRLLFt-2 | -0.0201 | -0.62 | -0.1778 | -2.51* | |

| Granger causality test | F-statistic | P-value | F-statistic | P-value | |

| H0: RLLF does not Granger cause LBKP | H0: LBKP does not Granger cause RLLF | ||||

| 0.8923 | 0.4114 | 2.0153 | 0.1361 | ||

On the right-hand side of Table 3, the coefficients of lagged terms ΔLBKPt-i are not statistically significant, and the Granger causality test also fails to reject the null hypothesis that LBKP does not Granger cause RLLF at the 5% significance level. The results generally show that Granger causality runs in no direction between LBKP and CME RLLF.

Table 4 presents the results of vector autoregressive (VAR) model between NBKP and RLLF, and Granger causality test. The results are exactly the same with those of VAR model between LBKP and RLLF, presented in Table 3. The results presented in Tables 3-4 suggest that the wood pulp and CME random length lumber futures are independent and there exists no correlation between them.

Table 4.

Results of vector autoregressive (VAR) model and granger causality

(NBKP vs. RLLF)

| Variable | ΔNBKPt | ΔRLLFt | |||

|---|---|---|---|---|---|

| Coefficient | t-statistic | Coefficient | t-statistic | ||

| Intercept | 24.9592 | 2.30* | 56.4672 | 2.25* | |

| ΔNBKPt-1 | 1.3220 | 19.70** | -0.0094 | -0.06 | |

| ΔNBKPt-2 | -0.3667 | -5.57** | -0.0279 | -0.18 | |

| ΔRLLFt-1 | 0.0165 | 0.54 | 1.1251 | 15.75** | |

| ΔRLLFt-2 | -0.0089 | -0.29 | -0.1814 | -2.55* | |

| Granger causality test | F-statistic | P-value | F-statistic | P-value | |

| H0: RLLF does not Granger cause NBKP | H0: NBKP does not Granger cause RLLF | ||||

| 0.4052 | 0.6674 | 0.6403 | 0.5283 | ||

3.4 Results of estimating cross hedge ratio and hedging effectiveness

Table 5 presents the results of the linear regression model estimated to obtain the risk-minimizing cross hedge ratio and hedging effectiveness. The estimated slope coefficients (β1) are 0.0112, 0.0194 respectively, and their correspondent t-statistics show that the estimated hedge ratios are not statistically significant. This implies that the movements in CME RLLF prices cannot explain the movements in wood pulp (LBKP and NBKP) prices.

Table 5.

Results of estimating cross hedge ratio and hedging effectiveness

| Variable | No. of Obs. | β0 | β1 | R2 |

|---|---|---|---|---|

| ΔLBKPt vs. ΔRLLFt | 197 | 0.2483 (0.93) | 0.0112 (0.32) | 0.0005 |

| ΔNBKPt vs. ΔRLLFt | 197 | 0.2645 (1.04) | 0.0194 (0.59) | 0.0018 |

On the other hand, R2s are 0.0005, 0.0018 respectively, indicating that the variation in wood pulp (LBKP and NBKP) prices is little explained by the variation in CME RLLF prices. The result suggests that the variation in wood pulp prices accounted for by the estimated regression model is not significant.

The above results, in general, suggest that CME RLLF cannot be used as a cross hedging vehicle for wood pulp. The results could be somewhat foreseen considering the distinct differences between wood pulp and CME lumber in terms of tree species (hardwood vs. softwood), usage (paper production vs. residential home construction), and the like.

4. Conclusions

The primary goal of this study is to determine the cross hedging potential of CME RLLF for wood pulp. The Johansen cointegration tests showed that wood pulp and CME lumber futures were not cointegrated. This suggests that there is no long-run equilibrium relationship between them. The results from Granger causality tests showed no evidence of a causal relationship between wood pulp and CME RLLF. This implies that there is no correlation between them. The results of the regression model also showed that the estimated hedge ratios were not statistically significant and the variation in wood pulp prices was not well explained by the variation in CME RLLF prices. As a conclusion, CME RLLF cannot be used effectively as a cross hedging vehicle for wood pulp.